Last updated:

Compound interest helps your money grow faster over time.

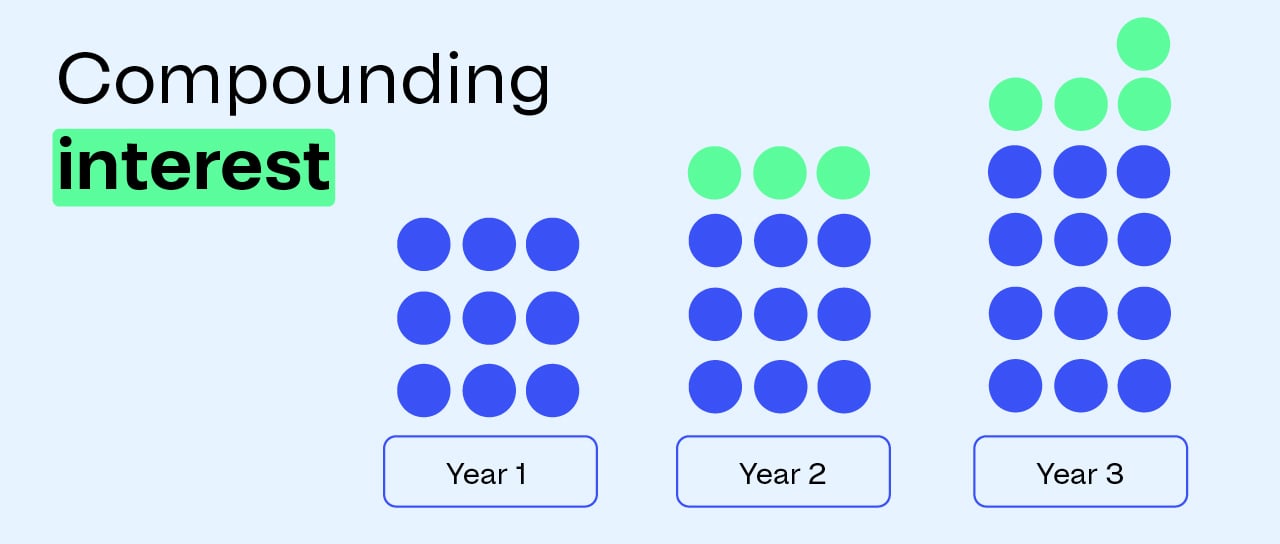

How compound interest works

When you put money in a savings account, super or investments, you earn interest on it and the balance can grow over time.

With compound interest, you earn on:

- your starting balance (called the principal), and

- the interest you've already earned.

This means you earn interest on your interest.

For example, in a savings account, your balance grows each time interest gets added. The next time interest is worked out, it's on your new, larger balance.

This is different from simple interest. Simple interest only applies to your starting amount. Some term deposits use simple interest.

Save more with compound interest

Compound interest can help your savings grow faster.

The longer you save, the more your balance can grow. So start early - it can make a big difference.

For example, if you put $10,000 into an account that pays 3% interest, compounded monthly:

- After 5 years, you'd have $11,616 (you'd earn $1,616 in interest).

- After 10 years you'd have $13,494 (you'd earn $3,494 in interest).

- After 20 years you'd have $18,208 (you'd earn $8,208 in interest).

Compound interest formula

You can use the compound interest formula to estimate how your money grows:

A = P x (1 + r)n

Where:

A = ending balance

P = starting balance (principal)

r = annual interest rate as a decimal (for example, 2% = 0.02)

n = how many times interest is added each year (for example, annually = 1, monthly = 12, daily = 365)

How to calculate compound interest

To calculate how much a starting balance of $2,000 will earn over 2 years at an interest rate of 5% per year, compounded monthly:

1. Find the monthly rate:

(0.05) x 12 (as interest compounds monthly) = 0.00416667

2. Find the number of periods:

2 years x 12 months per year = 24

3. Use the compound interest formula

A = $2,000 x (1 + 0.00416667)24

A = $2,209.88

Lorenzo and Sophia compare the compounding effect

Lorenzo and Sophia both invest $10,000 at a 5% interest rate for 5 years. Sophia earns interest monthly. Lorenzo earns interest at the end of the 5-year term.

After 5 years:

- Sophia has $12,834.

- Lorenzo has $12,500.

Sophia earns $334 more because she benefits from the compounding effect and earns interest on interest each month.

Join thousands of Australians and get tools, tips and calculators to help with your money - straight to your inbox each month.

Sign up